In the world of finance and investing there are plenty of gurus out there who will sell you all kinds of advice. I’ve seen it all and I’m sure you have too. There are the day traders who promise you can make a living sitting in your living room trading two hours a day. You’ll also read about the latest mutual funds with the greatest potential, poised for success this year. Then there are the penny stockers, the swing traders, and the option traders who all but promise 100% returns.

But the simple truth is that many success stories are from people following simple strategies and making them automatic. You see, financial success isn’t in the magic formula. It’s in the consistency. Sure, there are things you have to watch out for such as high fees, staying out of debt, and spending mindfully.

The secret to financial success isn’t in the magical formula but in the consistency.

But if you can follow a tried and true strategy faithfully and ignore the hype and promise of a glamourous ride to riches, your odds of success go up dramatically. And the secret to maintaining this course is to create a system of good financial habits and then automating them.

As you’re well aware, despite the best-laid plans, life gets in the way. There are kids to take care of. Extra bills always have a way of showing up when you least expect them. Surprise expenditures. It’s true, life is expensive and it’s easy to become side-tracked and allow our money to then be directed to other distractions.

Before you know it, you haven’t paid yourself first. Meaning, you haven’t set aside money for your future. And who can blame you? Life is in the now. There are plenty of things to deal with in the present, right?

But as we all know, if we don’t take care of our future as well as our present, our later prospects are going to be slim. Meager, in fact. I know people who have always taken care of their present and never set aside anything for their future. And now they’re suffering for it.

Saving money is not something that is generally intuitive and easy to do. It doesn’t spontaneously happen. So we have to use a little strategy and make it automatic.

So, just how powerful is automation and how do you implement it in your life? Are there any downsides to making things automatic? And, how beneficial is this system anyway?

Glad you asked!

How Does Automation Apply To Us?

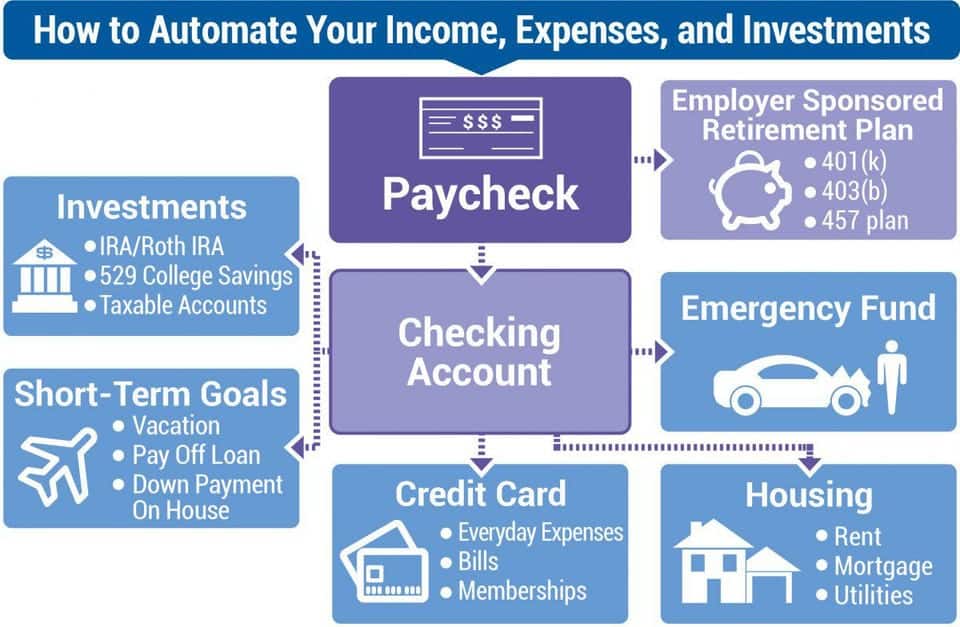

To start, let’s identify our definition and intent concerning financial automation. Simply, it’s using an electronic system(s) that directs and transacts where your money is going without your manual input every time. You set a system up and it takes over for you. You can then use this automation tool to assist your journey to financial independence. It takes some of the burdens off your plate.

Meaning, you don’t have to manually direct those dollars. Once the system is set up it does the heavy lifting for you.

Some examples of this are:

- Automatically paying your car payments

- Routine internet and TV streaming payments

- Regular monthly mortgage payment.

- Consistent additions to your emergency fund

- Automatic contributions to your 401(k)/403(b) or another similar plan.

- Regular contributions to a Roth IRA

Automate Your Bills

There are a few ways you can automate some of these.

Through your bank

One way is through your bank which is what I recommend. Here, you give your bank the account numbers of the payee. Then you determine how much and when you’re going to pay them. Everything is then handled through the bank – you’re not giving anyone access to your bank information. I believe this is a more secure (and easy once it’s set up) method.

Debit transactions

The other way is through automated debit transactions which I don’t recommend and should be considered with caution. Here, you are allowing a business to deduct money from your bank because you provided them your account information. Think about that: you have given them access to your bank! Mistakes can happen and by the time you find out money is already gone from your account. Then you have to invest the time (and hassle) to fix the mistake. However, with some institutions, this may be the only method of automation they offer so make sure it’s a well-known entity.

Credit cards

Another method is by paying via your credit cards. A lot of payees now accept credit card payments and this can be a great method because these cards offer protection concerning fraud to you (vs using a debit card). Plus you can get the bonus of reward points or cash back through your card. Sometimes, however, there can be an expensive transaction fee that is greater than any rewards the card may offer so pay attention to that detail!

And remember to always pay those credit cards off!

Automate your investments

The real powerhouse with automation is in our savings and investments! We’ll touch on the details in a bit, but this system is what will help propel you to financial success.

Overall, automation allows you to streamline your finances, assigning each dollar to a specific purpose month after month without you having to worry or forgetting about it. Your main job at this point is to monitor the accounts.

So, let’s get into some of the details, shall we?

How Do You Automate Your Finances?

Step 1: Get your budget set

Yep, it all rolls back to the budget, doesn’t it? Without it, you’re lost. You have to know what money is coming in and what is going out to know where to allocate funds for this to work. It’s the hub of your “cash-flow”.

The budget is the backbone of your finances.

So, go back to the basics and figure out all your income sources and expenses. And then assign each dollar a purpose. The benefit of this is that this will force you to review your finances, see where you’re overspending and where you can cut back. The goal, ultimately, is to free up some dollars. Then that money can be automated to contribute to your future self.

So, go back to the basics and figure out all your income sources and expenses. And then assign each dollar a purpose. The benefit of this is that this will force you to review your finances, see where you’re overspending and where you can cut back. The goal, ultimately, is to free up some dollars. Then that money can be automated to contribute to your future self.

Step 2: Open up bank accounts that have automated systems in place

The first step generally involves your checking account and your employer.

If you have an employer that offers a direct deposit (your paycheck gets automatically deposited into an account for you versus you cashing the check manually) then get this set up. This will make sure your money arrives in your bank on time and regularly.

Also, many banks nowadays offer various automated services. They will allow you to pay bills online and set these payments upon a set schedule. Remember, do this through your bank (so you’re giving the bank the account numbers) and not through the payee (meaning you’re giving them your bank routing number, etc). This is definitely an improved version of the old-school method of writing out checks for each bill!

Step 3: Put your bills on autopay

Set up each bill you have on the bank’s bill pay section if they offer it. This may take a bit of time to manually enter in each bill at first (the account numbers, etc), but once done, this will be a time saver for sure.

The first time you do this, I would recommend that you confirm that these bills actually get paid on time. Meaning, don’t assume you entered everything correctly the first time or that the system is flawless. Once you confirm the payment has gone through, you’re ready to go. Then set up the regular monthly “non-fluctuating” bills on an auto feature.

Tip: Some bills will be the same each month (such as auto and home insurance) and this makes it an easy solution. Others may have different monthly amounts (such as an electricity bill). You may have to manually adjust these monthly.

As previously mentioned, you may even be able to pay your bills via your favorite credit card to reap the reward points. Just check this out carefully since some banks will charge a fee to do this, negating any benefits. If you choose this route, pay those credit cards immediately afterward!

Again, this is a great point to review your monthly bills, setting up the essential bills to be paid first. Because the next step involves paying yourself which is incredibly important.

Warning: sometimes you can have these bills on auto-pay and accidentally end up over-drafting your account especially if you “forget” about any other auto-payments not associated through your bank (for example, a car payment through a separate loan agency you set up that gets deducted from your checking).

To help, you can often set up a separate savings account that is linked to this checking account as an overdraft feature. A word of caution here: they may charge you when they transfer money so beware. So it’s important to keep your budget on track!

Step 4: Automate your emergency fund

This is the step where you start taking care of yourself (after the essentials and before the accessories!). You can set up a separate savings account that is linked to your checking and automatically transfer funds. In some cases, you can have funds automatically transferred from your employer directly to a separate emergency fund account.

to your checking and automatically transfer funds. In some cases, you can have funds automatically transferred from your employer directly to a separate emergency fund account.

The intent, of course, is to start out with whatever you can but have a goal of eventually building up 3-6 months of living expenses. This “goal” may be intimidating, so start out with even $100 a paycheck if you can. This is then a less daunting task to accomplish. Then set it on auto, meaning those contributions happen, for instance, bi-weekly on a regular basis.

Then don’t touch the money unless you absolutely have to! Over time, those hundred-dollar contributions will add up. Preferably, you want to be aggressive in this step to build this account as fast as possible so shoot for more than the $100 bucks if you can! But if you have to, start with something, set it on automatic, and let it drip feed it for you.

Step 5: Automate your retirement accounts

This step helps you pay yourself first and is easier than it’s ever been in the past. Today, many employers offer 401(k) or 403(b) type accounts (depending on the type of institution you work for) that help you participate in the stock market. Often, these employers will automatically enroll you and deduct money from your paycheck into these funds. For example, my employer does this for new employees, pulling out 3% of their pay.

Of course, they give you the option to “opt-out” of this which I wouldn’t recommend. The goal, of course, is to get you to invest in yourself. With few pension-type plans around anymore, the burden is on you to prepare for your own future.

So, keep up this step especially if your employer offers a “match” on your dollars (where they contribute a certain percentage on your behalf) because this is free money to you.

You can also automate other financial accounts such as your IRA, Roth IRA, and even regular brokerage accounts. Just go to the area on the company’s website where you can set this up. It will then make recurring deposits from your checking account (so, yes, in this case, you may have to link it with your checking account). It’s easy to do and will be worth it in the long run.

Step 6: Increase the money in your investments automatically

There are even options where you can “automate” a raise of your contributions to your 401(k)/403(b) accounts each year. It’s as easy as going into your account and choosing this option if it’s available. Choosing a 1% increase will have that 3% grow to 4% the next year. Before long, you’ll be contributing 10%+ to your account which is a great goal.

The objective is to set it and forget about it.

That’s the best course at least concerning your actual contributions (I would suggest monitoring your portfolio!). Over time, these contributions will add up. I personally know people who don’t make a lot of money but they have amassed tens of thousands of dollars doing this. They just add a few additional dollars paycheck after paycheck.

Step 7: Take advantage of round-up tools

Some banks and a variety of apps now offer the ability to “round up” your daily expenses and deposit it into a savings account (or trading account) for you. For instance, if you spent $10.35, they will round up what is drawn from your checking to $11.00 and take that extra $0.65 and put it into these other accounts.

You may not think this is a big deal, but I’ve used this with both my personal bank and later with an app called Acorns. This initially helped to build up my savings account. Later I switched it to Acorns so that money could grow with the stock market.

These funds built up over time since it’s routine and automatic. This makes it easy for me!

The Dangers of Automating Your Finances

Sometimes there can be a bit of a disadvantage by automating your finances.

Danger #1: Ignoring your accounts

Sometimes it’s easy to become so automated that you don’t pay attention to your accounts. This is your money so you still need to pay attention! One thing that’s happened to me (and it could happen to you) is having things automated on many different platforms and accidentally overdrawn my checking account.

For instance, I had balanced out my checking and thought everything was good. Only a couple days later I got a text message from my bank stating I’d overdrawn the account. How you might ask? I had forgot about my auto-contribution to my online brokerage account (the one that was linked to my checking so I didn’t see it until after the fact). Yeah, dumb, I know. Out of sight, out of mind. But it happens. So pay attention!

Danger #2: Too many payments too soon

You might be asking, what do I mean? If you get paid bi-weekly you could accidentally schedule too many payments in one of the biweekly paycheck periods. Even though you should be paying attention to your budget and recognize this, it can still happen.

For myself, I wanted to start making serious payments to a larger debt. Although my monthly budget could tackle it, making that payment once a month on say, the 5th, seriously taxed that specific paycheck. The easy fix, of course, was to cut that payment in half, paying each every two weeks. Yep, grade-school math problem but if you miss it (which only takes once) you’re into an over-draft situation.

Also, be aware of scheduling payments a day or so before you actually get paid (or your check clears if manually depositing it). Checking in is important!

Danger #3: Missing out on your errors, fluctuating expenses, and possible fraud

Human error happens all the time. Fraud and identity theft also happen frequently. By automating, it’s easier to miss things if you’re not careful. Sometimes it’s easy to set something up as an auto feature and only realize later that it’s not working out after errors have been made.

easy to set something up as an auto feature and only realize later that it’s not working out after errors have been made.

For example, your auto insurance was adjusted and you failed to increase the payments to the auto feature at your bank. Unless you’re checking in often, things can get missed. And in the case of bills that fluctuate from month to month, it’s best to manually pay these through the banks’ bill-pay vs setting them up as an auto-pay.

Fraud can also be a problem if you don’t review your accounts. Sometimes it’s easy to become so automated that we don’t check our statements or review our transactions.

It’s easy to get lazy and just assume everything is ok.

You still have to stay connected to your money and check in on these accounts.

The Benefits of Automating Your Finances

Benefit #1: Convenience

I’m sure this is an easy one to see. Yep, it’s a little bit of a hassle to set your auto payments up initially, but the benefits soon outweigh the costs. It’s more convenient to pay those bills and to contribute to an emergency fund when it does all the work for you. Everything is on autopilot!

Another benefit is that you don’t have to remember when all those payments are due. And you don’t have to remember to fund that important Roth IRA!

Benefit #2: Your bills get paid regularly

Have you ever delayed paying that credit card payment because you’re waiting to see if there is money in the account at month’s end? Instead, figure out your budget and put this bill right now on autopay. Preferably as much as you can (more than the minimum if possible) then don’t decrease but increase the payment over time.

Credit card interest rates are very high so you need to pay these off as fast as possible. Make this a priority. This system will keep you consistent and you’ll hopefully not revert back to “minimum payments” since it’s now “hands-off”. You also don’t want to accidentally miss a payment and get charged a penalty. This will not only affect your financial future but will impact your credit score.

Benefit #3: You’ll regularly increase your emergency savings

Yes, this is important. Life throws curve balls at us all the time. The unexpected happens, whether it be car troubles, health issues, or a myriad of other surprises. Studies have shown that many people don’t have enough emergency savings. Having enough funds for an emergency situation can save you from financial disaster. This will help you to not use those expensive credit cards that drain your net worth.

Don’t focus on trying to save up to the six-months living expenses goal – that’s a massive number and will make the goal feel like its insurmountable. Which means you won’t want to do it. It’s better to tackle this in small steps.

For now, set a firm amount and regularly contribute. Then don’t touch it unless you absolutely have to. This will help guarantee that money will be going into your savings account on a regular basis. Increase it when you can (with your next pay raise!). Eventually, you’ll reach that goal.

The problem is with most people, they save this step to the last when they “have enough” at the end of the month. Guess what? You’ll always find a use for that money somewhere else if you don’t automate the process.

Leaving it as the last thing you do is a setup for failure. It’s too easy to only focus on the now and not think about it later. By automating the process, you’ll place this on a higher priority and ensures that you save the way you should be doing. Eventually, that goal will be reached.

Benefit #4: This can make you wealthy

Ok, now we’re talking, right? Well, maybe. You see, there are no guarantees in all of this, but the likelihood of your success is greater when you implement the power of automation.

Not only are you routinely paying your bills, but automation can help you pay off that debt that’s been plaguing you for years. That is if you get aggressive with using automation to its fullest. Meaning, you pay as much as you can then set it on auto so it hammers away at it paycheck after paycheck. This means you’ll eventually be debt-free! Then get serious and keep yourself that way.

Not only are you routinely paying your bills, but automation can help you pay off that debt that’s been plaguing you for years. That is if you get aggressive with using automation to its fullest. Meaning, you pay as much as you can then set it on auto so it hammers away at it paycheck after paycheck. This means you’ll eventually be debt-free! Then get serious and keep yourself that way.

Then as you begin to invest, having things automatic also propels your progress. If you only contribute to your Roth IRA when you feel you have enough money, you simply won’t do it for very long.

Set it on automatic instead. $100 every biweekly paycheck will contribute $2,600 a year. Then with every raise you get, take a part of it and increase those contributions! Pretty soon you can be maxing out that Roth IRA which is a great idea!

This can do miraculous things for your finances. Don’t believe me? Let’s take a look at someone’s 401(k).

Take the average 30-year-old and have them retire “early” at 65 (yep, gone are the days when the “normal” retirement age was 65, it’s now 67!). Let’s say they’re making $50,000 per year and contribute 10% of their salary each year growing at an average of 8% a year. Over this time period, this person could make almost $1,329,000!

Nice and impressive, correct? Now instead have that person increase those contributions with their raises automatically every year (that’s the benefit of automatic increases, it gets done, no need to remember) and that situation changes dramatically.

Assume they had the same scenario but now let’s take 30% of every raise (about 1% of every 3% raise in this case set on an auto feature) each year and add to those contributions to a max of 15% of their pay (although why stop there if you can afford it!).

Now that account could grow to over $2,046,000! That’s $717,000 more because of the “auto” increase combined with the “auto” contributions!

We all know that market gains are not guaranteed, but the idea behind using automation to propel your financial success is sound. What’s also true is this: left to ourselves doing this manually, we’re usually going to find other uses for that money and your retirement can certainly suffer because of it.

Automate As Much As You Can Concerning Your Finances

When you automate your finances you’re giving your dollars a purpose from the start. Whether that purpose is to take care of the monthly bills, pay down debt, or build your future, those dollars have intention behind them. It’s routine management without a second thought. Believe it or not, your stress over your future will be less because you know you’re in fact building that future. This will help you build financial independence.

Will everything be perfect or can you walk away and forget about it? Definitely not. But when you automate your finances you can save and plan for a future with more control. And that brings peace of mind!

Latest posts by David the Wealthy RN (see all)

- Five Negative Aspects of the 401(k) - July 19, 2023

- How To Think About Bear Markets - April 8, 2023

- Live Paycheck to Paycheck the Right Way! - December 26, 2022